The global payments landscape stands at a crossroads. Traditional cross-border payment systems—reliant on correspondent banking networks and SWIFT messaging—have remained largely unchanged for decades, despite mounting evidence of their inadequacy for the modern digital economy. Transactions take one to three business days to settle, costs remain stubbornly high at an average of 6.3% of remittance values, and the lack of transparency leaves payers and recipients in the dark about fees, exchange rates, and delivery times.

These inefficiencies stem from structural realities. The correspondent banking model requires multiple intermediaries, each maintaining separate accounts, conducting independent compliance checks, and operating within different time zones and regulatory frameworks. The result is a fragmented, opaque system where information and value flow along separate paths.

Central Bank Digital Currencies (CBDCs) offer a transformative alternative. By digitizing central bank money and embedding it in programmable platforms, CBDCs can fundamentally reimagine how value moves across borders. But realizing this vision requires solving a critical challenge: interoperability — the ability of different CBDC systems to work together seamlessly.

The Interoperability Imperative

The 2024 BIS survey on CBDCs reveals the scale of global interest: 91% of the 93 central banks surveyed are actively exploring CBDCs, with wholesale CBDC experimentation advancing rapidly. Yet each jurisdiction approaches CBDC design differently, reflecting local priorities, legal frameworks, and technological preferences. Without interoperability, these national systems risk becoming isolated digital islands—exchanging information and value no more efficiently than today’s fragmented infrastructure.

The G20 roadmap for improving cross-border payments has identified interoperability as a priority, recognizing that the full benefits of CBDCs will only materialize through coordinated international action. The question is not whether CBDC systems should connect, but how.

Three Models of CBDC Interoperability

Analysis of recent cross-border CBDC experiments reveals three distinct architectural approaches to interoperability, each with unique characteristics, trade-offs, and suitable use cases.

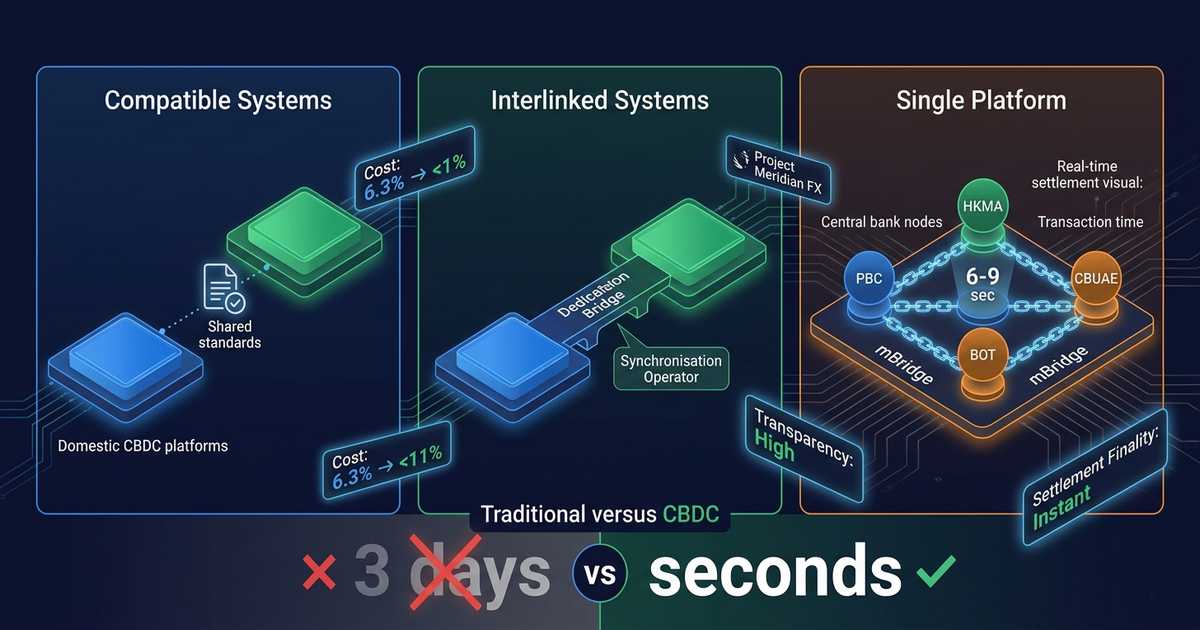

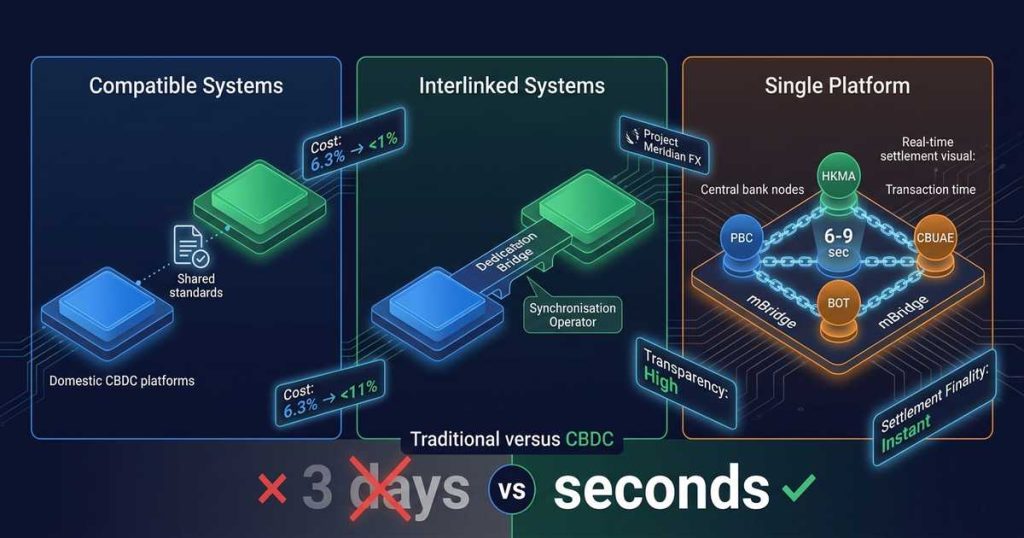

📊 Model 1: Compatible Systems

The compatible systems model represents the least intrusive approach to interoperability. Participating jurisdictions agree on common standards—technical protocols, data formats, regulatory requirements, and legal frameworks—while maintaining separate, domestically-focused CBDC systems. Transactions flow across borders through bilateral arrangements, with each system translating and validating according to shared rules.

Key Example: Project Helvetia

Led by the Bank for International Settlements (BIS), Swiss National Bank, and SIX, this project explored how wholesale CBDCs could integrate with existing core banking systems through compatible design. Phase II demonstrated that integration is operationally possible, addressing practical complexities around settlement and legal frameworks.

Advantages ✅

- Minimizes disruption to existing financial infrastructure

- Central banks retain full control over domestic systems

- Aligns with traditional payment system evolution (e.g., ISO 20022 standards)

Limitations ⚠️

- Transactions still traverse multiple systems with independent cycles

- Effectiveness depends on depth of agreed standards

- Significant coordination challenge given diversity of CBDC designs globally

🔗 Model 2: Interlinked Systems

The interlinked systems model creates dedicated connections between otherwise independent CBDC platforms. Through shared technical interfaces or common clearing mechanisms, value moves directly from one system to another without passing through multiple intermediaries.

Key Examples

- Project Stella: Joint experiment by ECB and Bank of Japan exploring interlinking between distributed ledger platforms

- Jasper-Ubin: Bank of Canada and Monetary Authority of Singapore demonstrating DLT system connections through common clearing mechanisms

- Project Meridian FX: BIS Innovation Hub project developing “synchronisation operator” (SO) connecting RTGS systems across jurisdictions

Advantages ✅

- Reduces intermediation chains while preserving national autonomy

- Accommodates different technological choices

- Enables direct value transfer through bilateral/multilateral agreements

Limitations ⚠️

- Scalability constrained by number of bilateral connections required

- Hub-and-spoke arrangements introduce governance challenges

- Each new participant requires new agreements and integrations

🌐 Model 3: Single Multi-Currency Platform

The most ambitious interoperability model consolidates multiple CBDCs within a unified platform. Rather than connecting separate systems, participating central banks issue their digital currencies onto a shared infrastructure, where they coexist and transact according to common rules. Transactions occur directly between participants on the platform, with settlement finality provided by the underlying distributed ledger technology.

Key Examples

- Project mBridge: Most advanced implementation. Expanded from Hong Kong-Thailand to include China and UAE. Entered MVP phase in June 2024 with real-value transactions.

- Project Dunbar: BIS Innovation Hub with Australia, Malaysia, Singapore, and South Africa developing shared multi-CBDC platform prototypes.

- Project Jura: Bank of France and Swiss National Bank testing cross-border settlement using euro and Swiss franc wholesale CBDCs on single DLT platform.

Technical Architecture (mBridge)

- Each central bank as a validation node on distributed ledger

- Commercial banks operating standard nodes

- HotStuff Plus consensus mechanism for transaction finality

- Smart contracts enabling programmable compliance checks

- Average settlement time: 6-9 seconds (vs. days in traditional systems)

Advantages ✅

- Greatest efficiency gains — transactions complete in seconds

- Full transparency and finality

- Smart contracts enable automated compliance

- Direct settlement between commercial banks

Limitations ⚠️

- Deepest integration and highest trust among participants required

- Complex governance questions: platform access, regulatory differences, secure infrastructure sharing

- Monetary sovereignty concerns require careful architectural choices (e.g., limiting redemption rights to domestic banks)

Comparative Analysis: Three Models at a Glance

| Dimension | Compatible Systems | Interlinked Systems | Single Platform |

|---|---|---|---|

| Integration Depth | Low | Medium | High |

| National Control | Full | High | Shared |

| Efficiency Gain | Moderate | Significant | Transformative |

| Complexity | Low | Medium | High |

| Governance Requirements | Standards coordination | Bilateral/multilateral agreements | Shared platform governance |

| Key Projects | Helvetia | Stella, Jasper-Ubin, Meridian FX | mBridge, Dunbar, Jura |

The choice among models involves fundamental trade-offs. Compatible systems preserve maximum national autonomy but deliver limited efficiency improvements. Single platforms offer transformative gains but require unprecedented levels of international cooperation and trust. Interlinked systems occupy the middle ground, balancing integration with independence.

The Geopolitical Dimension

Interoperability is not merely a technical challenge — it carries profound geopolitical implications. Traditional cross-border payments rely heavily on the SWIFT messaging network and the US dollar’s dominant role in trade and finance. This concentration creates strategic dependencies and, as recent sanctions have demonstrated, potential vulnerabilities.

CBDC interoperability initiatives, particularly those involving China and other major economies, are sometimes viewed through a geopolitical lens. The mBridge project, with its Chinese participation and focus on reducing reliance on traditional infrastructure, exemplifies this dynamic. Some observers anticipate that interoperability platforms may initially develop along regional lines, reflecting existing trade relationships and strategic alignments.

Yet the underlying motivation for most central banks remains practical: faster, cheaper, more transparent payments benefit all economies. The BIS continues to emphasize multilateral cooperation, with projects like Meridian FX demonstrating how traditional RTGS systems can interoperate with newer DLT-based platforms regardless of the currencies or jurisdictions involved.

The Road Ahead: From Experimentation to Reality

Key Milestones Achieved

- Multiple projects across three continents have demonstrated technical feasibility

- Validated architectural approaches for all three interoperability models

- Identified critical governance questions requiring international coordination

- mBridge MVP status — real transactions with real central bank money on shared platform

Remaining Challenges

- Legal alignment: Jurisdictions must recognize digital currencies and DLT-based settlement finality

- Data privacy: Requirements vary significantly across regions, demanding creative architectural solutions

- Governance arrangements: Must balance efficiency with accountability for shared platforms

- Monetary sovereignty: Preventing undesired accumulation of domestic currency by foreign entities

Future Outlook

- Pluralism rather than single dominant model: Different corridors may adopt different approaches

- Regional platforms: Likely to emerge among closely integrated economies

- Interlinking clusters: Regional platforms will connect over time

- Compatible standards: Enable broad interoperability for global commerce

Conclusion

Central bank digital currencies hold genuine promise for transforming cross-border payments. By embedding money in programmable platforms and designing for interoperability from the outset, central banks can overcome the fragmentation, opacity, and delay that have long plagued international transactions.

The three interoperability models — compatible, interlinked, and single platform — represent a spectrum of integration, each suited to different contexts and objectives:

- Compatible systems offer a low-barrier entry point for jurisdictions seeking cross-border functionality while preserving domestic flexibility.

- Interlinked systems balance integration with autonomy, enabling direct value transfer without full platform convergence.

- Single platforms deliver transformative efficiency for participating currencies but demand deep trust and sophisticated governance.

As experimentation yields to implementation, the choices central banks make about interoperability will shape not only the efficiency of cross-border payments but also the broader architecture of the international monetary system. The technology is ready. The question now is one of collective will.