The Security Fragmentation Problem

Every new blockchain or decentralized service faces the same existential challenge: bootstrapping security. A proof-of-stake network requires billions of dollars in staked capital to become economically secure. A new rollup, oracle network, or bridge must either build its own validator set from scratch or rely on trusted third parties. The result is a fragmented security landscape where small networks remain vulnerable, and capital is siloed across isolated systems.

Restaking emerged as a solution to this fragmentation. Introduced by EigenLayer in 2023, restaking allows Ethereum validators to “re-stake” their already-staked ETH to secure additional networks called Actively Validated Services (AVS) . In exchange for providing security to these services, validators earn additional yield—on top of their existing staking rewards.

The concept has sparked one of Ethereum’s most transformative—and contentious—debates. Proponents see restaking as the foundation of “shared security”: a unified security layer where capital can be deployed efficiently across countless services. Critics warn of systemic risk: cascading failures where one AVS’s vulnerability compromises the entire Ethereum validator set.

This article examines restaking’s implications for Ethereum’s validator ecosystem—the economic incentives, operational dynamics, centralization pressures, and long-term sustainability of shared security models.

Restaking Mechanics: How It Works

At its core, restaking is a mechanism for reusing staked ETH as collateral across multiple services.

The Staking Foundation

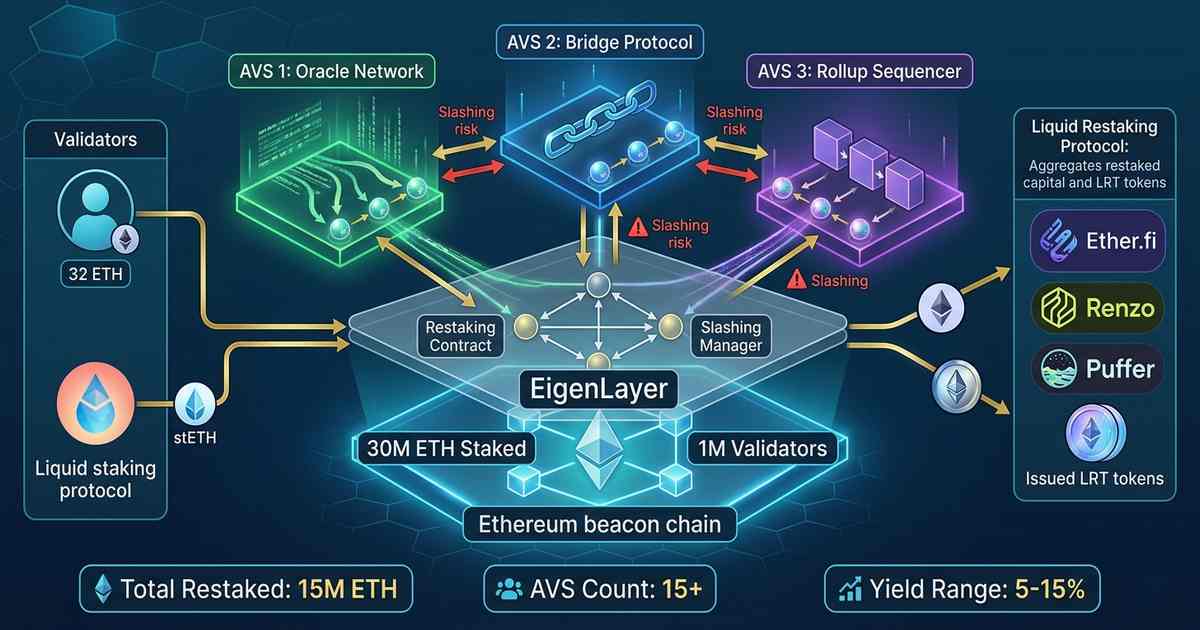

Ethereum’s proof-of-stake secures the beacon chain with approximately 30 million ETH staked across 1 million validators (as of early 2025). Validators earn approximately 3-5% annual yield for fulfilling their duties: proposing blocks, attesting to blocks, and participating in consensus.

Restaking via EigenLayer

EigenLayer introduces a new layer of contracts that enable validators to opt-in to restaking. Validators delegate their staked ETH to EigenLayer, which can then slash that ETH if the validator misbehaves on any AVS they choose to secure.

The process works as follows:

Native restaking: Solo stakers running 32 ETH validators can set EigenLayer as a withdrawal address, signaling their intent to restake. Their validator becomes eligible to secure AVS.

Liquid restaking: Liquid staking tokens (LSTs) like stETH, rETH, and cbETH can be deposited into EigenLayer to become “restaked.” Liquid restaking protocols like Ether.fi, Renzo, and Puffer Finance aggregate LST deposits and distribute them across AVS, issuing liquid restaking tokens (LRTs) in return.

AVS selection: Validators (or the LRT protocols representing them) choose which AVS to opt into. Each AVS sets its own slashing conditions—the behaviors that would trigger a penalty. By opting in, validators agree to be slashed on their staked ETH if they violate that AVS’s rules.

Yield accrual: AVS pay fees—typically in their own tokens or ETH—to validators for securing their networks. Restakers earn these fees plus their base staking rewards.

Slashing: The Disciplining Mechanism

Slashing is the mechanism that ensures validator accountability. If a validator misbehaves on Ethereum (e.g., double signing), they lose up to 1 ETH of their stake. Under restaking, misbehavior on an AVS could also trigger slashing—the AVS operator requests a penalty, and EigenLayer verifies the misbehavior before slashing the validator’s restaked ETH.

The possibility of multiple slashing vectors creates new risks. A validator securing five AVS faces five distinct slashing conditions. A bug in one AVS’s slashing logic, or a malicious AVS operator, could result in validators being slashed for violations they did not commit.

Shared Security: The Value Proposition

Shared security proponents argue that restaking solves fundamental inefficiencies in crypto-economic security.

Capital Efficiency

Traditionally, securing a new network required dedicating capital exclusively to that network. A validator with 32 ETH could either secure Ethereum or secure a new oracle network—not both. Restaking enables the same capital to secure multiple networks simultaneously, increasing capital efficiency by an order of magnitude.

For new projects, restaking offers a path to security without bootstrapping a validator set. Instead of issuing inflationary rewards to attract stakers, they can pay fees to existing Ethereum validators—leveraging Ethereum’s established security at a fraction of the cost.

Composability and Interoperability

Shared security creates a unified trust layer. If multiple AVS trust the same underlying validator set, they can interoperate with reduced trust assumptions. A bridge secured by restaked ETH inherits Ethereum’s economic security; a rollup secured by restaked ETH can trust that bridge without additional collateral.

Yield Diversification for Validators

For Ethereum validators, restaking offers additional yield streams. With base staking yields declining as more ETH is staked, restaking provides an alternative revenue source. Early restaking yields reached 20-30% for early adopters; as the market matures, yields may settle in the 5-15% range—still substantial supplements to base rewards.

The Validator Ecosystem: Who Restakes?

Restaking has created new tiers within the validator ecosystem:

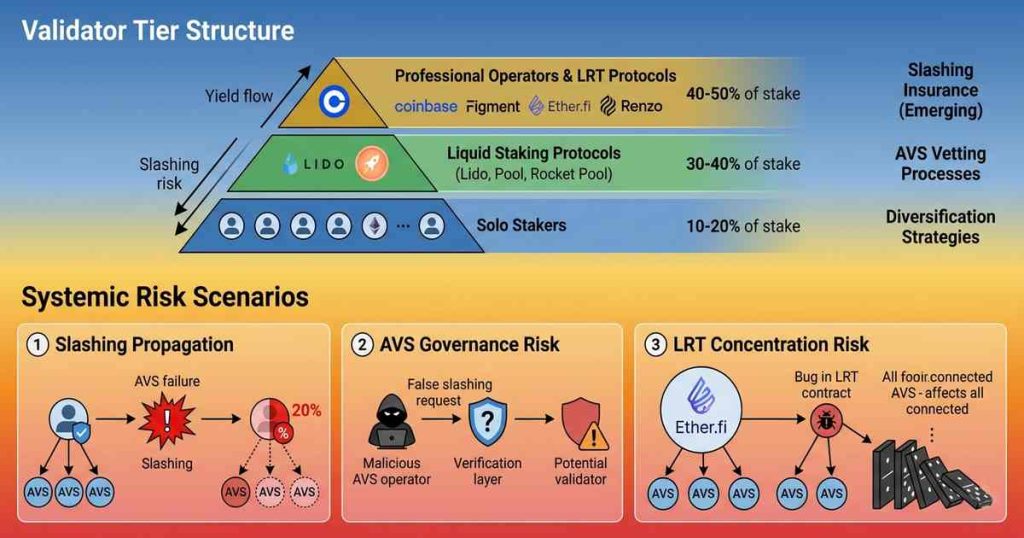

Solo Stakers

Solo stakers—individuals running 32 ETH validators—can natively restake by pointing their withdrawal address to EigenLayer. However, solo stakers face operational complexity: they must evaluate and select AVS, monitor slashing conditions, and manage multiple reward streams. Few solo stakers have the technical capacity or time to actively manage restaking.

Liquid Staking Protocols

Lido, Rocket Pool, and other liquid staking protocols manage hundreds of thousands of validators. These protocols are now offering restaking options, allowing their stETH or rETH holders to opt into restaking through LRT protocols. This creates new revenue for liquid staking protocols but also introduces slashing risk that ultimately falls on LST holders.

Liquid Restaking Protocols

A new class of protocols—Ether.fi, Renzo, Puffer, Kelp, and others—aggregates LST deposits and manages restaking across AVS. These protocols issue LRTs that represent claims on restaked assets. They actively manage AVS selection, slashing risk, and yield distribution. LRTs have become the primary vehicle for retail participation in restaking, with tens of billions in deposits.

Professional Validator Operators

Large institutional validators and staking-as-service providers (e.g., Coinbase, Kraken, Figment, Kiln) have embraced restaking. These operators have the resources to evaluate AVS, monitor slashing conditions, and manage complex restaking portfolios. They also hold significant influence over which AVS receive restaked security.

Centralization Pressures

Restaking introduces several centralization vectors that threaten Ethereum’s validator distribution.

The LST-LRT Concentration

Liquid staking protocols, particularly Lido, already control a significant portion of staked ETH. Liquid restaking compounds this concentration. LRT protocols aggregate deposits from LST holders, giving them outsized influence over AVS allocation. A small number of LRT protocols—Ether.fi, Renzo, and Puffer—now control a majority of restaked ETH.

Operator Consolidation

AVS require reliable, responsive validator operations. Solo stakers often cannot meet the uptime and responsiveness requirements that AVS demand. As a result, AVS preferentially select professional validator operators with proven infrastructure. This tilts restaking rewards toward institutional operators, potentially reducing solo staker participation.

Veto Power Concentration

Under EigenLayer’s architecture, AVS can set “operator sets” that determine which validators can secure them. AVS with strict operator requirements effectively exclude solo stakers and small operators, concentrating security provision among a few large entities.

MEV and Restaking Interaction

Maximal extractable value (MEV) already concentrates rewards among sophisticated operators. Restaking adds another reward layer that also favors sophisticated operators. The combination of MEV and restaking rewards could widen the gap between professional and solo validators.

Systemic Risk: Cascading Failures

The most significant concern with restaking is systemic risk: the possibility that failure in one AVS compromises the entire Ethereum validator set.

Slashing Propagation

If a validator is slashed on an AVS, they lose a portion of their restaked ETH. If that validator was securing multiple AVS, the slashing reduces the capital available to secure those AVS. In a worst-case scenario, a coordinated attack or bug could cause mass slashing across many validators, reducing the total ETH securing the beacon chain.

Correlation of Risks

AVS may be correlated. A bridge and a rollup both rely on the same oracle data; a failure in that oracle could cause both AVS to trigger slashing simultaneously. If many validators have opted into both services, a single failure could cause correlated slashing across the validator set.

Governance Capture

AVS govern their own slashing conditions. A malicious or compromised AVS could attempt to slash validators without cause. While EigenLayer includes verification mechanisms, governance attacks remain a risk. If an AVS accumulates sufficient restaked capital, its token holders might have influence over EigenLayer governance itself.

The LRT Amplifier

LRT protocols amplify systemic risk by concentrating deposits. A bug in an LRT protocol’s slashing management could affect thousands of depositors simultaneously. The failure of a major LRT protocol could trigger a cascade of withdrawals, destabilizing the AVS that rely on its restaked capital.

Economic Implications

Restaking fundamentally alters the economics of Ethereum staking.

Yield Competition

AVS must compete to attract restaked capital by offering attractive yields. This competition could drive yields higher, benefiting validators. However, high yields also attract risk-seeking capital, potentially encouraging AVS to offer unsustainable yields that eventually collapse.

Base Staking Yield Impact

As restaking offers additional yield, the opportunity cost of not restaking increases. Validators may be incentivized to restake regardless of their risk assessment, simply to remain competitive. This could lead to higher restaking participation than would be optimal from a risk perspective.

Demand for ETH

Restaking increases demand for ETH because restaking requires staked ETH. This demand could support ETH’s price and increase the total value securing the network. However, it also creates a feedback loop: higher ETH prices increase security, which encourages more restaking, which increases ETH demand.

Regulatory Considerations

Restaking operates in a regulatory grey area. Validators earning yield from AVS may be engaging in securities offerings or unlicensed brokerage activities. LRT protocols issuing tokens representing claims on restaked assets may fall under securities regulation.

The SEC and other regulators have shown interest in staking-as-a-service and liquid staking. Restaking adds another layer of complexity that may attract regulatory scrutiny. The classification of LRTs, the status of AVS tokens, and the role of restaking protocols in custody and delegation all remain unresolved.

The Future of Restaking

Several developments will shape restaking’s evolution:

Maturation of AVS market: The AVS ecosystem is nascent. Mature AVS will have proven security track records, clear governance, and sustainable business models—reducing risk for validators.

Slashing insurance: Insurance products that protect validators against slashing events could emerge, reducing risk for smaller participants and enabling broader participation.

Restaking interoperability: Multiple restaking protocols (EigenLayer, Symbiotic, Karak) are competing for market share. Interoperability standards could emerge, allowing restaked capital to move between protocols.

Regulatory clarity: Clear regulatory frameworks would enable institutional participation, potentially expanding the restaking market while imposing compliance costs that advantage larger operators.

Technical improvements: EigenLayer’s roadmap includes features like “programmable slashing” and “atomic slashing” that could improve security but also add complexity.

Conclusion

Restaking represents both an opportunity and a risk for Ethereum’s validator ecosystem. It offers capital efficiency, additional yields, and a path to shared security that could accelerate innovation across the Ethereum ecosystem. It also introduces centralization pressures, systemic risk, and economic complexity that could undermine the very decentralization that makes Ethereum valuable.

The validator ecosystem will adapt. Solo stakers may find their role diminished unless tools and protocols emerge to make restaking accessible without requiring professional infrastructure. Liquid restaking protocols will face pressure to demonstrate security and resilience. AVS will compete for capital, forcing trade-offs between yield and risk.

Ethereum’s security has always been a shared resource—validators securing the network collectively. Restaking extends this concept, inviting validators to share their security more broadly. Whether this extension strengthens or destabilizes Ethereum will depend on how the ecosystem manages the tensions between efficiency and safety, concentration and decentralization, innovation and stability.

The experiment is young. The outcomes are not yet written. But restaking has already transformed how we think about security in decentralized systems—and the implications for validators will unfold for years to come.